Homeowners in the United States are currently in a sensitive position as 2025 comes to a close and they prepare for the upcoming year. They face significant concerns over personal finances and rising costs, although there is less worry about broader trends, such as inflation, unemployment, and the political environment, based on our research.Homeowners show a cautiously engaged mindset. Strong intent persists with planned activity concentrated in maintenance projects.

What Trends are Driving Homeowner Readiness in the Home Improvement Industry?

Tighter budgets, rising remodeling costs, and stagnated incomes are influencing homeowner readiness within the home improvement industry in 2025, with many hesitant to take on large, high-end remodels and renovations at the moment and many choosing smaller DIY projects instead.Here is a look at some of the top home improvement trends that are currently shaping homeowners’ perspectives on home improvement and are likely to have an impact in 2026:

1. Home Improvement Products Market Shows Steady Growth

Based on data from HIRI’s Q2 2025 U.S. Home Improvement Products Market Forecast, spending in the home improvement products market is expected to increase 2.5% in 2025, with an average 4% annual growth rate from 2026-2029, reaching roughly $688 billion by that year. From a homeowner perspective, the DIY products market saw a modest increase in 2024 and is expected to increase 1.3% in 2025. Growth is projected to be stronger in the consumer market in the upcoming year. The fastest-growing markets for homeowner spending are Alaska, Washington, the District of Columbia, Colorado, and North Dakota.

We always witness seasonal cycles for sales in building materials, garden equipment, and supplies with more retail sales taking place from April to November. Advanced retail sales for building materials, garden equipment, and supplies dealers decreased in August, down 7% from July, according to HIRI’s October Economic and Industry Update. Compared to the same period last year, advanced retail sales are down about 5.7%.Additionally, HIRI’s Quarterly Homeowner Project Activity Tracker shows that while big-box retailers remain the dominant channel for purchasing home improvement products, local hardware stores gained notable traction throughout 2025, with about one-third of DIY homeowners reporting that they shopped for products and materials through this channel during the third quarter, up from 21% in the same quarter last year.

2. Concern of Trade Policy and Tariffs has Eased

Trade policy uncertainty has eased in recent months but remains elevated in a historical context. Trade policy uncertainty tends to reduce investment spending in industries heavily exposed to trade in input and output markets. Amid ongoing policy uncertainty, firms have initially managed increased costs by either depleting pre-tariff inventories or absorbing margin reductions (or both). This has resulted in a partial pass-through to consumer prices, but not at an alarming rate. However, the two latest CPI reports indicate that businesses are willing to pass the increased costs directly to consumers, but perhaps in stages as they become more confident about where tariff rates will ultimately settle. We anticipate this trend will continue in the coming months and become more apparent in 2026 data.While recent attention has centered on tariffs’ impact on goods prices, services inflation remains the primary driver of overall inflation. As a general trend, our outlook expects commodity prices will remain relatively weak globally into early 2026. In the U.S., several commodities face higher-than-usual premiums compared with other economies because of tariffs. However, imports from some regions into the US remain competitive even with 50% tariffs.

3. Inflation, Unemployment, and Consumer Confidence Impact Economic Outlook

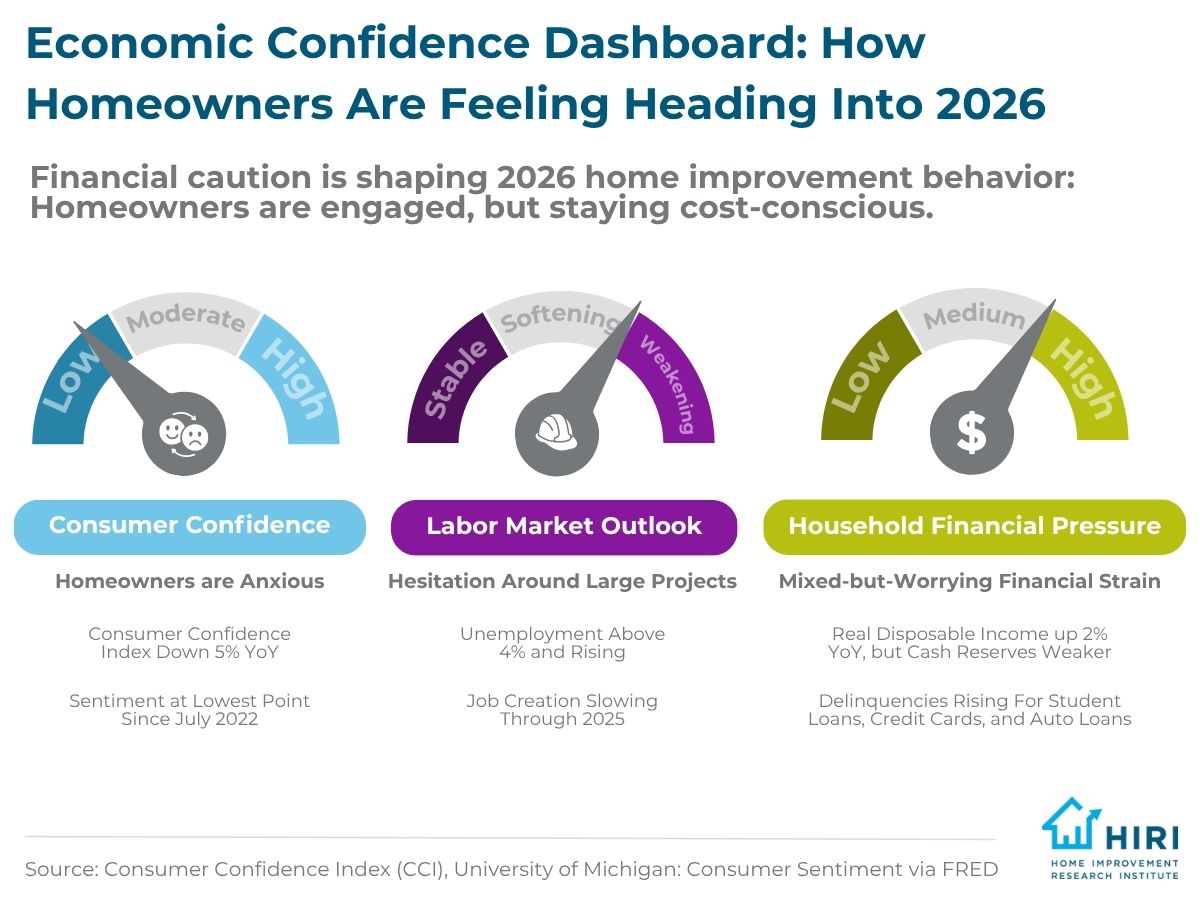

Other important economic indicators also provide insight into where homeowners and households currently stand financially. Unemployment is higher than 4%, and the number of jobs added to the economy has been decreasing in the back half of 2025. This is part of a long-term trend, with significantly fewer jobs being created in the U.S. Additional uncertainty stems from the country’s current policy. This includes the federal government layoffs, many of which occurred earlier this year. With many employees still receiving severance, they will not be counted as unemployed until October and will start to be reflected in forthcoming datasets. A tougher stance on immigration has severely reduced border crossings and increased deportations, potentially constraining labor supply in sectors like construction that rely on immigrant workers.Throughout the year, consumer confidence has been notably low, based on the Consumer Confidence Index (CCI). In September, the CCI was down 5% from the same month last year. Consumer sentiment, as tracked by the University of Michigan, has also remained low this year, and is currently at the lowest rate since July 2022.

4. Household Income Drives Home Improvement Spending

One positive economic indicator, as revealed in data from HIRI’s Economic and Industry Update from October 2025, is that real disposable personal income (RDPI) remained stable in August, and year-over-year disposable income is also up nearly 2% from August 2025. Yet while income inched upward, weaker cash reserves and slower debt reduction has reinforced household anxiety. These pressures have been steering priorities toward affordability, smaller undertakings, and deferred discretionary spending. Relative to income, debt balances are lower than they were before the pandemic. Rising auto loan and credit card delinquencies have slowed, and the transition rate for mortgages, the largest share of household debt, remains near its pre-pandemic level. That said, delinquency rates for student loans are rising quickly and remain elevated for credit card and auto loans. Therefore, it bears watching for signs that the added financial strain is spilling over into other credit products as we head into 2026.

5. Housing Inventory Improves but Sales are Struggling

Activity in the housing market provides important home improvement statistics that give insight into what DIY homeowners are experiencing and their willingness to undertake various projects. In recent memory, the lack of homes listed for sale has been one of the main storylines in the US housing market, but, that story has changed markedly in 2025. The active inventory of homes for sale is now above levels a year earlier in nearly all states and major metro areas, with total US inventory more than 20% higher. Home sales, meanwhile, are not keeping pace, exerting downward pressure on prices and giving some leverage to buyers. Additionally, according to the Economic and Industry update, homeownership dipped slightly in Q2 2025. Compared to last year, homeownership has decreased 0.6%. All regions (Northeast, Midwest, South, and West) are down compared to last year.Builders have responded by cutting prices and heavily promoting incentives, like rate buy-downs, to keep completed home inventory moving. Home builders are projected to start 1.32 million homes in 2026. In 2026, home sales are expected to continue to be tempered due to the locked-in effect: with existing homeowners with low-interest-rate mortgages feeling stuck, and much of first-time homebuyers being priced out the market. The bright news is that overall home sales are forecasted to bounce back up to 4.39 million in 2026 as homes become more affordable due to lower mortgage rates and lower real home prices from supply-demand pressures.

6. Homeowners Prioritize Maintenance and Low-Risk Projects

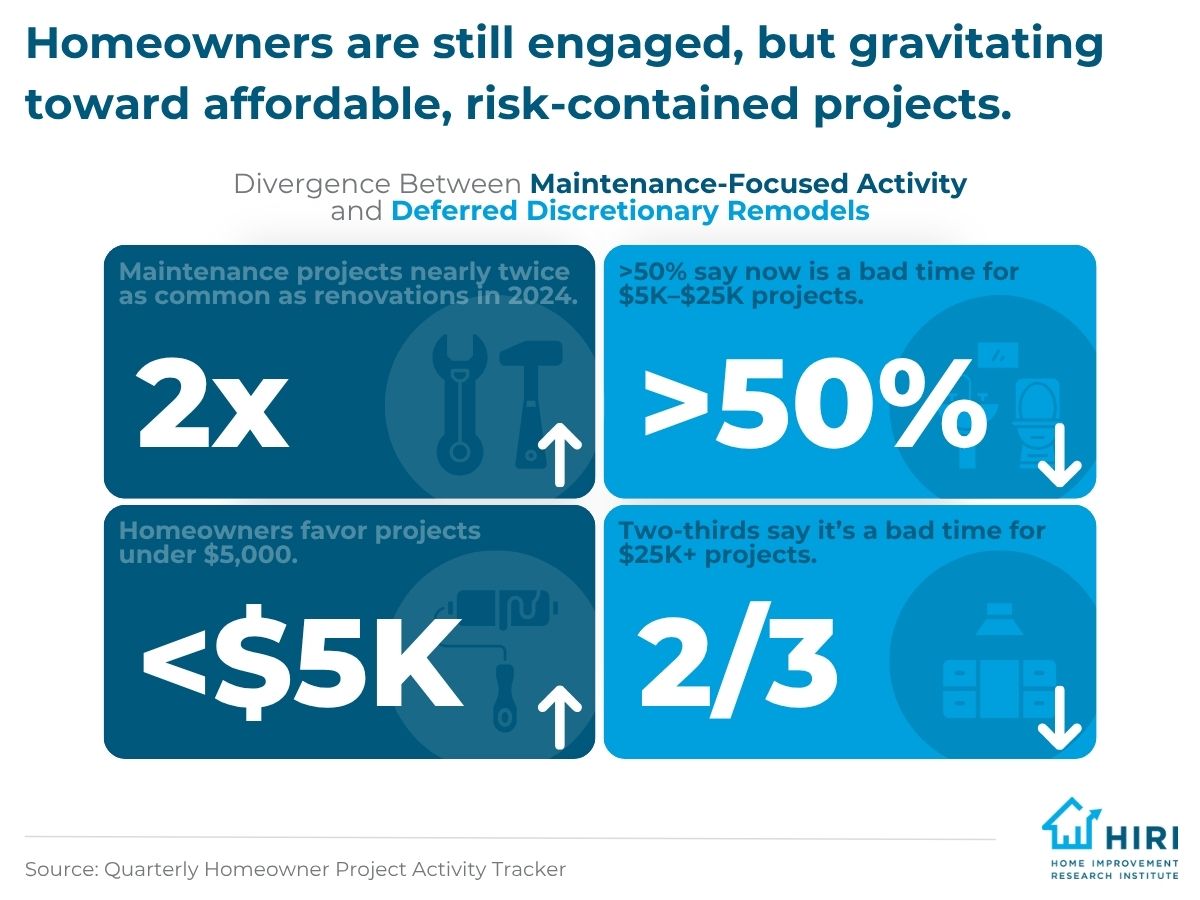

In light of financial strain and cooling optimism, DIY trends reveal that homeowners are focused on essential maintenance and lower-risk projects, underscoring a retreat from discretionary ambition. Throughout 2024, home maintenance including routine tasks and activities to keep a home in good condition, were the most popular types of home improvement projects completed, and nearly twice as popular as home renovations across all four quarters. Budgets, labor costs, and overruns have been reinforcing cost as the central barrier to these shifts in home improvement behaviors. Motivations also center on income gains, economic conditions, and incentives, but affordability is the dominant factor.

7. Pro Engagement is Changing, with Selective Hiring

Professional contractors and tradespeople have availability right now. The number of construction jobs decreased more than 34% between July and August, and they’re down approximately 70% from last year, according to our Economic and Industry Update. However, after a rough second quarter, data shows that contractor business confidence is growing.Further, data from our Quarterly Homeowner Project Activity Tracker shows that slightly more homeowners turned to pros in Q3 for expertise and specializations on complex projects, yet smaller-scaled projects leaned DIY, led by the desire to save on costs. Fewer kitchen and bath hires signaled that rising bath activity was largely DIY-drivers, reflecting selective, need-based professional use.

8. DIY Homeowners are Moderating Planned Spending

Planned spending for 2026 fell below past-year levels, landing between essential and discretionary categories, signaling greater caution on larger, non-essential upgrades. Based on home remodeling statistics from our research, safety, mobility, and rental income are gaining traction as motivations for home improvement projects, alongside steady priorities to optimize comfort and home values. In light of macro financial concerns, individuals are finding ways to tighten their budgets. Most homeowners are planning to spend less on dining, entertainment, vacations, and hobbies in 2026, but only about one-quarter of households plan to spend less on home improvement activities. The majority of homeowners are prioritizing spending on home improvement above other discretionary categories, even if that spending is still likely to be centered on projects costing less than $5,000. In general, more than half of DIY homeowners feel it’s a bad time to start a project between $5,000 and $25,000 and nearly two-thirds feel it is a bad time to start a project that is $25,000+.

9. Project Priorities are Shifting

Over the past quarter, we’ve observed some shifts in types of home improvement projects, some of which may be expected as the seasons change. The exterior-heavy activity reported in quarter 2 shifted indoors in the third quarter, with baths and whole-home systems advancing. There was also a heavier focus on living spaces, such as family rooms, dens, and playrooms. Large yard and garden projects bucked the seasonal slowdown, while tighter finances redirected focus from mid-scale outdoor work toward manageable interior projects. Looking ahead to what products homeowners intend to purchase in the next few months, the research shows that they favor practical, aesthetic upgrades, such as furniture, appliances, paint and landscaping, which reflects lingering caution on large discretionary projects.

Gaining Insight into Homeowner Readiness Trends

To learn more about homeowners’ current perspectives on home buying and home improvement, as well as how financial concerns and economic uncertainty influence their inclination to take on new projects, download our most current Quarterly Homeowner Project Activity Tracker and Economic and Industry Update. As a member of the Home Improvement Research Institute, you will gain access to not only this research, but other data and insights on both professional customers and DIY consumers to help guide your business strategies in the coming year.