Understand purchase incidence and spend behavior by product.

Edit

Edit

Pro Remodeling Product Purchase Trends

Biennial Contractor Product Purchase Incidence Study & Analysis

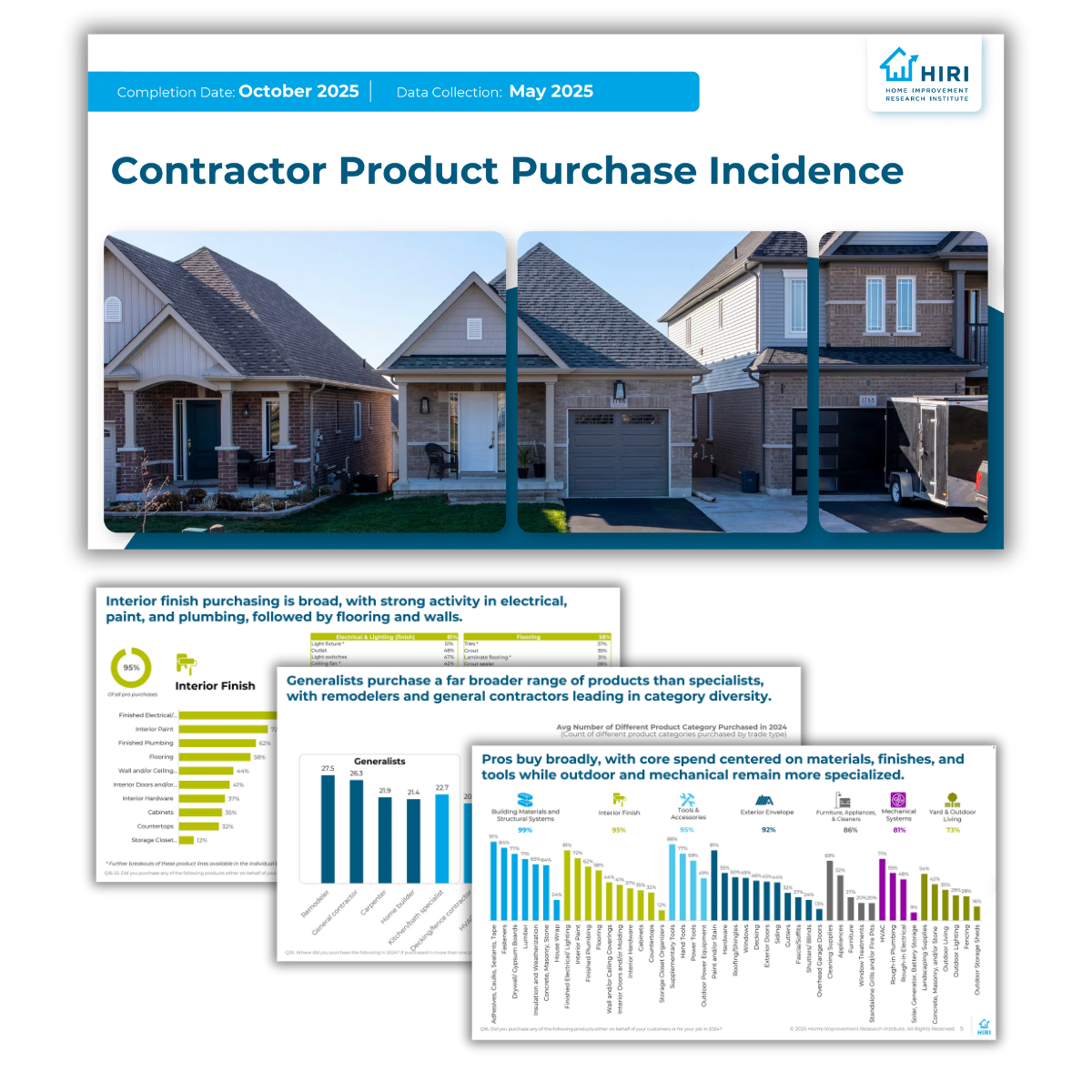

Every other year since 1999, the Home Improvement Research Institute has surveyed home improvement remodelers and specialty contractors to track critical product and channel activities. This study outlines the product purchases of professional contractors with product details in 6 product categories including: Building Materials & Structural Systems, Exterior Envelope, Furniture Appliances & Cleaners, Interior Finish, Mechanical Systems, and Tools & Accessories.

Objectives

Identify suppliers used for purchases by product.

Analyze attachment and cross-product opportunities

Download Report Overview

Download Building Materials and Structural Systems Specific Report

Download Exterior Envelope Specific Report

Download Furniture, Appliances, and Cleaners Specific Report

Download Interior Finish Specific Report

Download Mechanical Systems Specific Report

Download Tools and Accessories Specific Report

Download Yard and Outdoor Living Specific Report

FAQs

What analysis exists on contractor paths to purchase in the home improvement industry?

The Home Improvement Research Institute's biennial Contractor Product Purchase Tracking Study explores purchase incidence and spending behavior among industry professional on a product level. It also includes data about the suppliers used for purchases. Based on data from the report, digital channels heavily influence buying, as industry professionals rely on retailer websites and search engines for specs, inventory, and reviews, expecting complete, accurate, and easily comparable product data online. However, there are some variations in how and where contractors purchase products and materials, based on the category.

HIRI's Contractor Product Purchase Tracking Study outlines the product purchases of professional contractors with details in six core product categories including Building Materials and Structural Systems; Exterior Envelope; Furniture Appliances and Cleaners; Interior Finish; Mechanical Systems; and Tools and Accessories. The analysis in these detailed reports will help home improvement industry stakeholders understand and track the differences and similarities for pro purchasing behaviors across these various product categories.

What are the latest trends in how contractors purchase home improvement products?

Contractors purchase home improvement products broadly, with core spend centered on materials, finishes, and tools while outdoor and mechanical remain more specialized. According to the Home Improvement Research Institute's biennial Contractor Product Purchase Tracking Study, cleaning and appliance purchases highlight pros’ continued role in post-install and maintenance work that extends beyond just homeowner purchases.

Overall, demand patterns suggest a stable, full-spectrum purchasing ecosystem where essential materials anchor spend and adjacent categories (finishes, mechanicals, and outdoor living) offer incremental growth opportunities. Another recent trend is that generalists purchase a far broader range of products than specialists, with remodelers and general contractors leading in category diversity. Across trades, adhesives and supplementary tools are shared staples, while trade-specific materials define differentiation.

Are contractors buying more home improvement products online or in stores?

Contractors continue to buy a majority of their home improvement products in stores. Big-box retailers capture the bulk of pro spend across nearly all product categories, especially interior finishes, and power tools. However, specialty suppliers remain essential for complex, high-skill categories like HVAC and electrical, where expert service and support drive loyalty, based on the Home Improvement Research Institute's biennial Contractor Product Purchase Tracking Study.

Together, these patterns underscore a price-conscious but brand-loyal market where accessibility and reliability outweigh experimentation. Direct-from-manufacturer purchasing remains limited, strongest in windows; solar, generator, and battery storage; adhesives, caulk, sealants, and tape; and cabinets.

Additionally, local building material stores remain competitive in core structural and exterior categories, including lumber, drywall, and siding. For professional contractors, online channels remain small but growing, driven by convenience categories, such as tools, furniture, and HVAC supplies.

What motivates contractors to choose certain home improvement brands?

Contractors’ brand choices hinge on proven performance and product reliability. Innovation matters less than consistent quality, warranty coverage, and on-time availability across key materials and tools. Based on findings in the Home Improvement Research Institute's biennial Contractor Product Purchase Tracking Study, the most important attributes when choosing a certain home improvement brand are quality and durability, followed by availability, price, and ease of installation.

Digital channels heavily influence buying among contractors. Pros rely on retailer websites and search engines for specs, inventory, and reviews, expecting complete, accurate, and easily comparable product data online. Not only does HIRI's report outline purchase incidence and spend behavior by product, but the data can help to identify suppliers used for purchases by product and also analyze attachment and cross-product opportunities.

What are the main differences between DIY and contractor home improvement purchase trends?

Both DIY and contractors purchase broadly across home improvement product categories. Professionals’ purchase decisions remain pragmatic and efficiency-driven, as they are typically purchasing products in larger quantities and for planned projects. Quality, durability, and product availability anchor brand choice, while sustainability and innovation trail as secondary factors, based on data from the Home Improvement Research Institute's biennial Contractor Product Purchase Tracking Study.

For the DIY homeowner market, at least half annually purchase products from every building category, except for Exterior Envelope and Mechanical Systems, according to the most recent data from the Home Improvement Research Institute's biennial Homeowner Product Purchase Tracking Study.

Both of HIRI's tracking studies outline home improvement purchase trends in six core product categories including Building Materials and Structural Systems; Exterior Envelope; Furniture Appliances and Cleaners; Interior Finish; Mechanical Systems; and Tools and Accessories. The data can be used to identify the main differences between DIY and contractor home improvement purchase trends.

Additionally, HIRI's quarterly U.S. Size of the Home Improvement Products Market Report & Forecast breaks down spending over the past five years for various product categories by both the consumer and professional markets. It also provides five-year forecasts for both groups.

Edit

Related Reports

Not a Member Yet?

Explore free articles, infographics, and webinars to get even more value from HIRI

Enter a valid email address

There was an error

Thanks for subscribing!

Research

Resources

About Us

© 2026 Home Improvement Research Institute. All rights reserved.